[ad_1]

You may be in the market for a new credit card for various reasons. Perhaps you want a new welcome bonus or the opportunity to earn valuable rewards from your daily purchases. Others look for new credit cards to achieve a “good” credit score.

If you’re applying for a credit card to improve your credit score, it’s important to understand how your new account will affect you.

While there are several ways a new credit card can help your credit score, there are also some pitfalls to watch out for. Otherwise, opening a credit card could result in a temporary or long-term decline in your credit score.

Let’s discuss three ways a well-maintained credit card account can improve your credit score.

reduce credit utilization

Perhaps the biggest benefit to be gained from new credit cards is the potential for lower overall credit utilization. Credit utilization is a term that describes the percentage of your credit card limit that is in use. The lower your credit usage, the higher your credit score.

A new credit card comes with a new credit limit. If you already have other open credit cards with outstanding balances, the new account may cause a drop in credit utilization.

Of course, the best way to reduce your credit usage is to pay off your credit card balance. However, if you cannot afford to zero your credit card, requesting a higher credit limit or opening a new credit card may help in the short term. You may also consider using a balance transfer credit card as a way to consolidate and reduce credit usage at the same time.

establish a good payment history

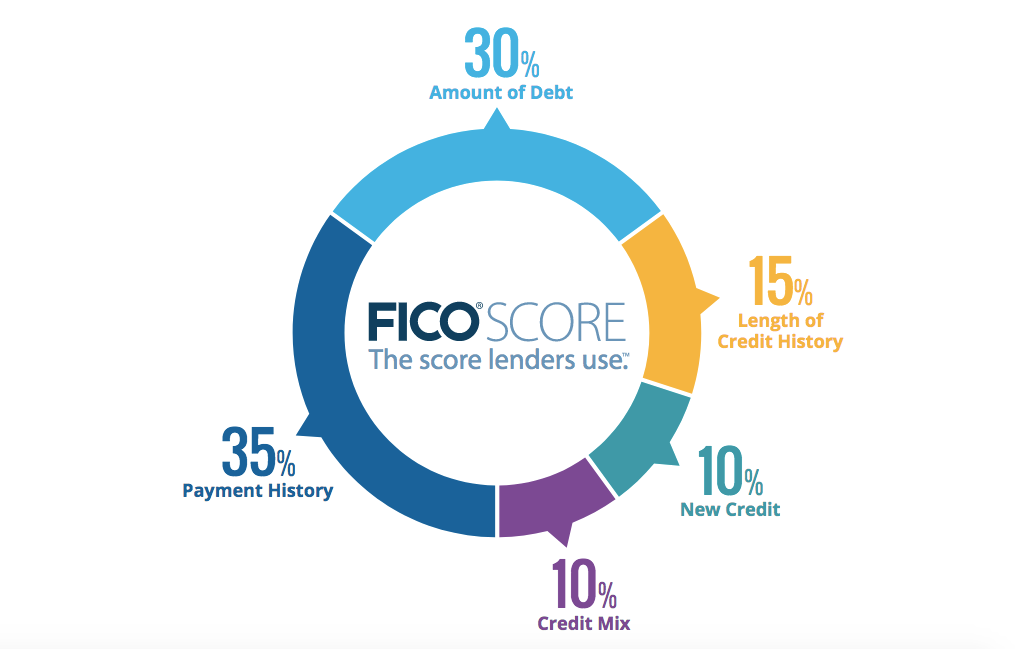

Another way a new credit card can help your credit score is by helping you build a good credit history. Payment history accounts for 35% of FICO scores and 41% of VantageScore credit scores. So if you open a new credit card and always pay on time, your account will help you establish a strong payment history over time.

Additionally, if you only have a few accounts on your credit report, you may benefit from opening a new credit card. If your credit file is “thin” (less than 5 credit accounts), you may have trouble getting a mortgage, renting an apartment, or opening a cell phone account.

Sign up for our daily newsletter

Related: Why paying your credit card balance is more important than ever

Diversification of credit mix

New credit cards can improve your credit score by adding account diversity to your credit report. Credit scoring models such as FICO and VantageScore pay attention to many details of your credit report.

One of the factors these scoring models evaluate is the combination of account types they have experience managing (also known as the credit mix). Credit mix equals 10% of FICO score and 20% of VantageScore.

There are two main categories of credit accounts: installment and revolving. Installment credit typically includes mortgages, auto loans, student loans, and personal loans. Revolving credit includes credit cards and lines of credit. A mix of these accounts on your credit report can result in a high credit score.

If you’ve never had a credit card before, adding a credit card to your credit report may improve your credit score. However, if you already have other revolving credit cards on your credit report, you probably shouldn’t expect additional credit score increases in this area.

Credit score pitfalls to avoid when opening a new credit card

- Late payment: Always pay on time. Late payments can hurt your good credit score. Additionally, negative information, such as late payments, can remain on your credit report for up to seven years.

- High credit utilization: A high balance-to-limit ratio tends to negatively impact your credit score. Additionally, rolling an outstanding credit card balance month to month usually also pays high interest. We recommend that you pay the balance of your statement in full each month.

- Claiming too many accounts: Don’t be nervous about applying for a new credit card when you want to take advantage of attractive offers. However, too many inquiries in a 12-month period can hurt your credit score.

- Opening too many new accounts: Opening a new credit card lowers the average age of accounts. This can lower your credit score in the short term. Also, opening many new accounts at once, by credit card or otherwise, can have a significant negative impact on your score.

- Closure of old accounts: It’s generally not a good idea to close an old credit card just because you opened a new one. Closing old credit cards (especially accounts with zero balances) can increase overall credit utilization and lower your credit score.

Conclusion

A new credit card can often help improve your credit score if you open an account and use it responsibly. However, it is important to always pay on time. Additionally, we recommend paying off your credit card balance in full each month.

RELATED: TPG’s 10 Commandments of Credit Card Perks

Also, consider reviewing three credit reports to check your credit standing before applying for a new account. Knowing where your credit is can help you shop around for the best credit card for your situation.

[ad_2]

Source link