[ad_1]

Finally, some good news. With inflation rising at a moderate rate for now and positive CPI inflation, 10-year yields should drop significantly and with it mortgage rates! has been reached and the Fed is nearing the end of its rate hike cycle. Let’s look at today’s data.

From the Consumer Price Index report: The U.S. Bureau of Labor Statistics released today’s Consumer Price Index (CPI-U) for all urban consumers rose 0.4% in October on a seasonally adjusted basis, the same rate as September. Over the last 12 months, the all-commodity index increased by 7.7% on a non-seasonally adjusted basis.

The consumer price index data estimate was for 7.9% year-on-year growth. Some in the market speculated that the data was going to be even hotter than expected, with some whispering numbers pointing to growth of 8.2% to 8.4% year-over-year. people have come to believe that bond yields and mortgage rates will be much higher than they are today.

However, this report was 7.7%, lower than expected.As a result, mortgage interest rates 7.37% yesterday 6.67% As of this writing.

10-year yields will rise sharply Thursday morning, bond yields will fall (see above), and today’s mortgage rates will fall below 7%. One year makes a big difference. I’m thrilled that mortgage rates are now below his 7%. But it makes sense given that mortgage rates have ranged from 3.14% to 7.37% over the past 52 weeks.

One of my issues with the inflation data is that the biggest driver of core inflation is shelter and this data line lags behind. We are currently crawling CPI data, lagging behind August 2020 when it was still down.

We already have the latest data lines showing that inflation growth is stabilizing.A few federal reserve Members have commented on the fact that they are aware of Shelter’s inflation data on CPI lag. This is positive. Some people feared the Federal Reserve didn’t understand her CPI data lag, but that doesn’t seem to be the case.

So you have to understand that the CPI shelter data is lagging and the cooldown is a story for 2023, especially in the second half of this year. CNBC He made this point before the CPI report was released, explaining that although shelter inflation had a foot in growth, it was unable to sustain growth.

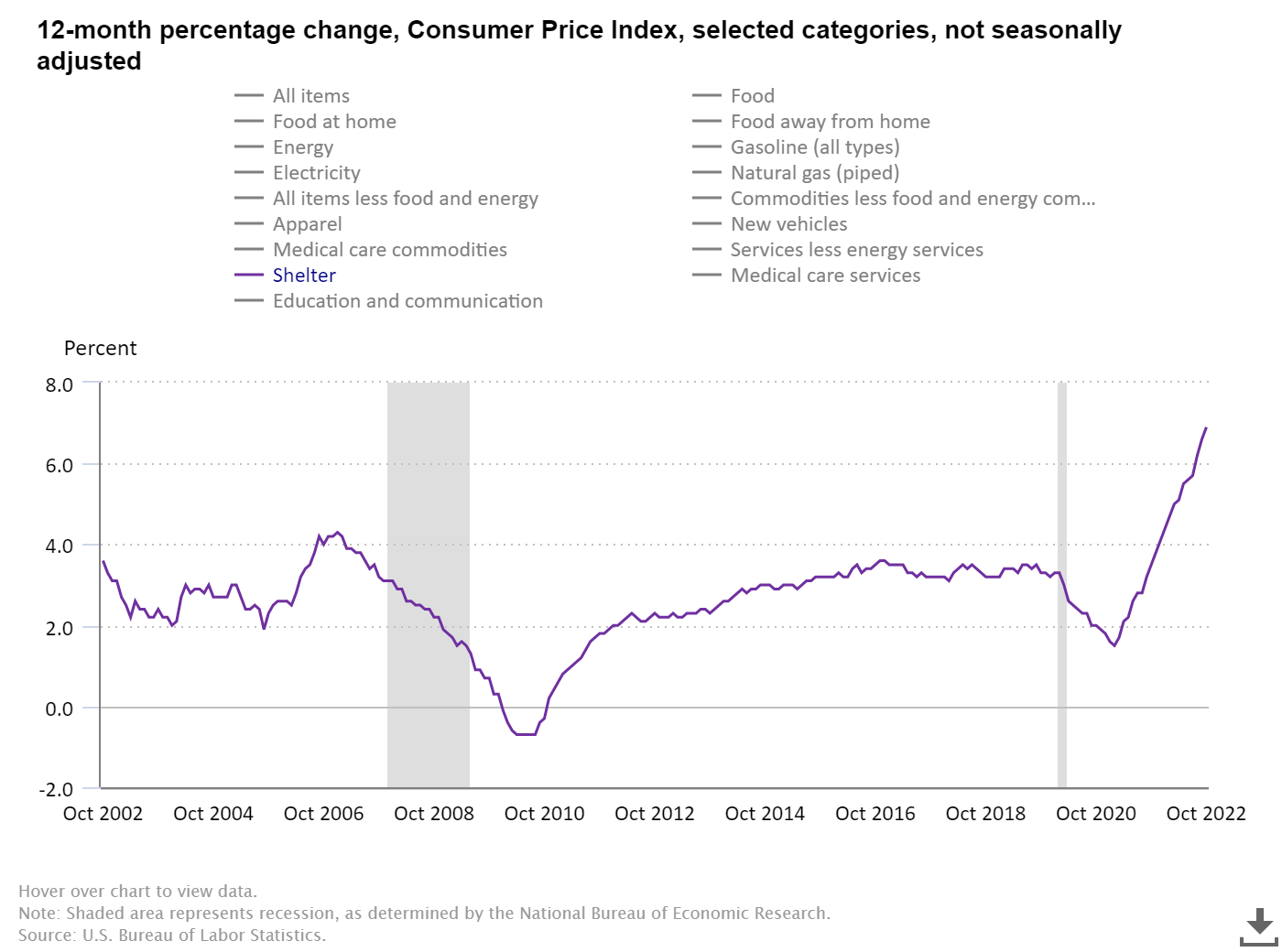

Shelter CPI Inflation Data

As you can see in the chart below, Shelter inflation has risen and may continue to rise. One thing to remember is that 910,000 two-unit homes are expected to come online in 2023, which will help slow inflation growth next year. More recent data lines already show an increase in shelter cooling, so this could be a positive story for 2023.

When this data line starts to cool, core inflation will be the biggest factor in cooling. This is why I wrote about how we need to root for better home completion data to increase supply to the market.The best way to deal with housing inflation is to increase supply. That being said, there are many two-unit constructions in the pipeline.

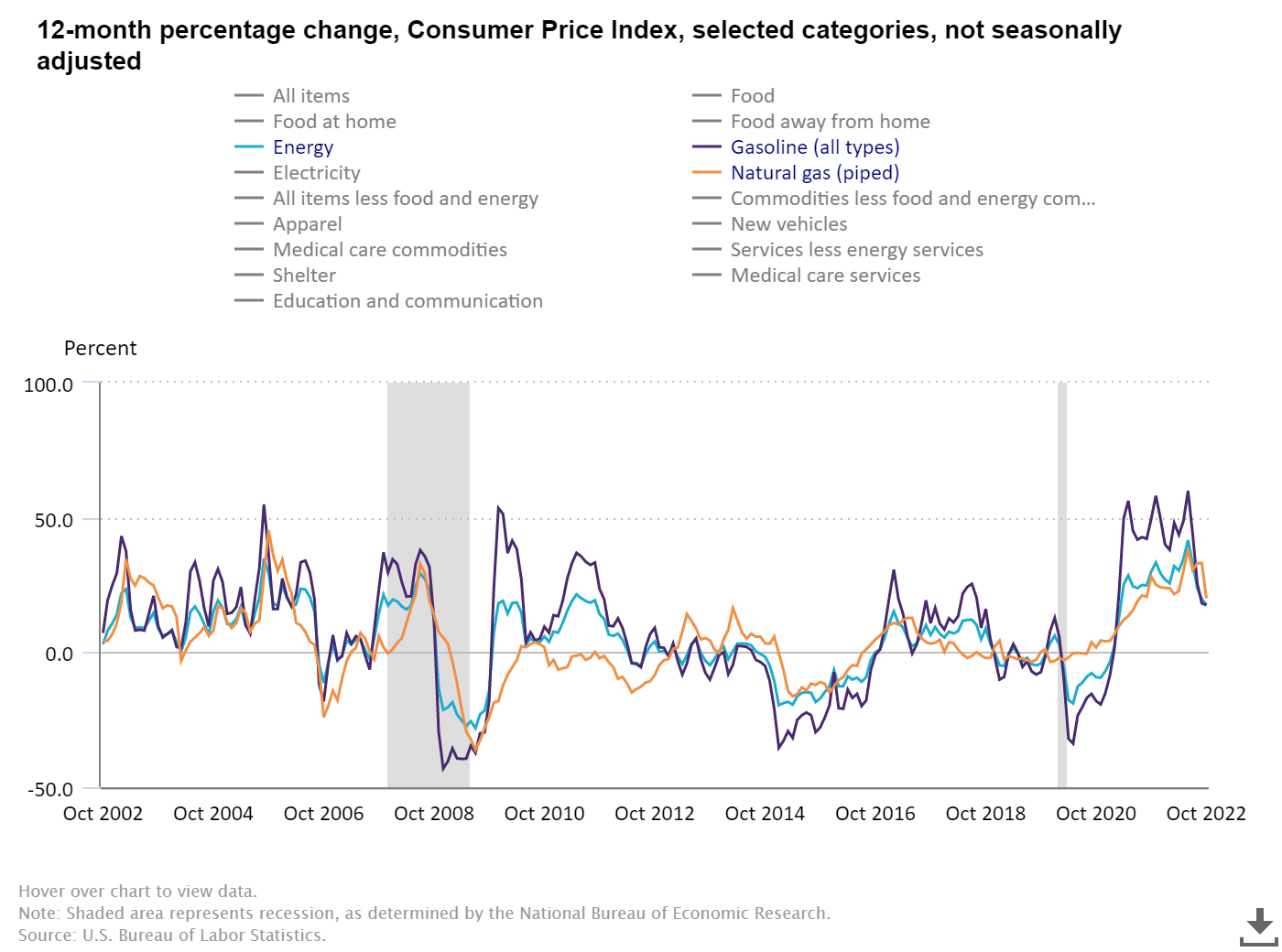

Some inflation data have cooled off from recent peaks. Food and energy are not part of the core inflation data as they can be highly variable. As you can see below, the Mad Max Inflation Basket growth has slowed, mainly because energy prices have dropped from their recent highs.

Other inflation data are also cooling. We all know used car prices have exploded as supplies have plummeted during the pandemic. It has already changed and there is room to lower it. If you’re trying to keep inflation down by killing demand and losing jobs, the market doesn’t have adequate supply.

The history of global pandemics traditionally means that supply chains will be stressed for two years.Now that we are free to roam the planet, production supply levels are returning to normal.

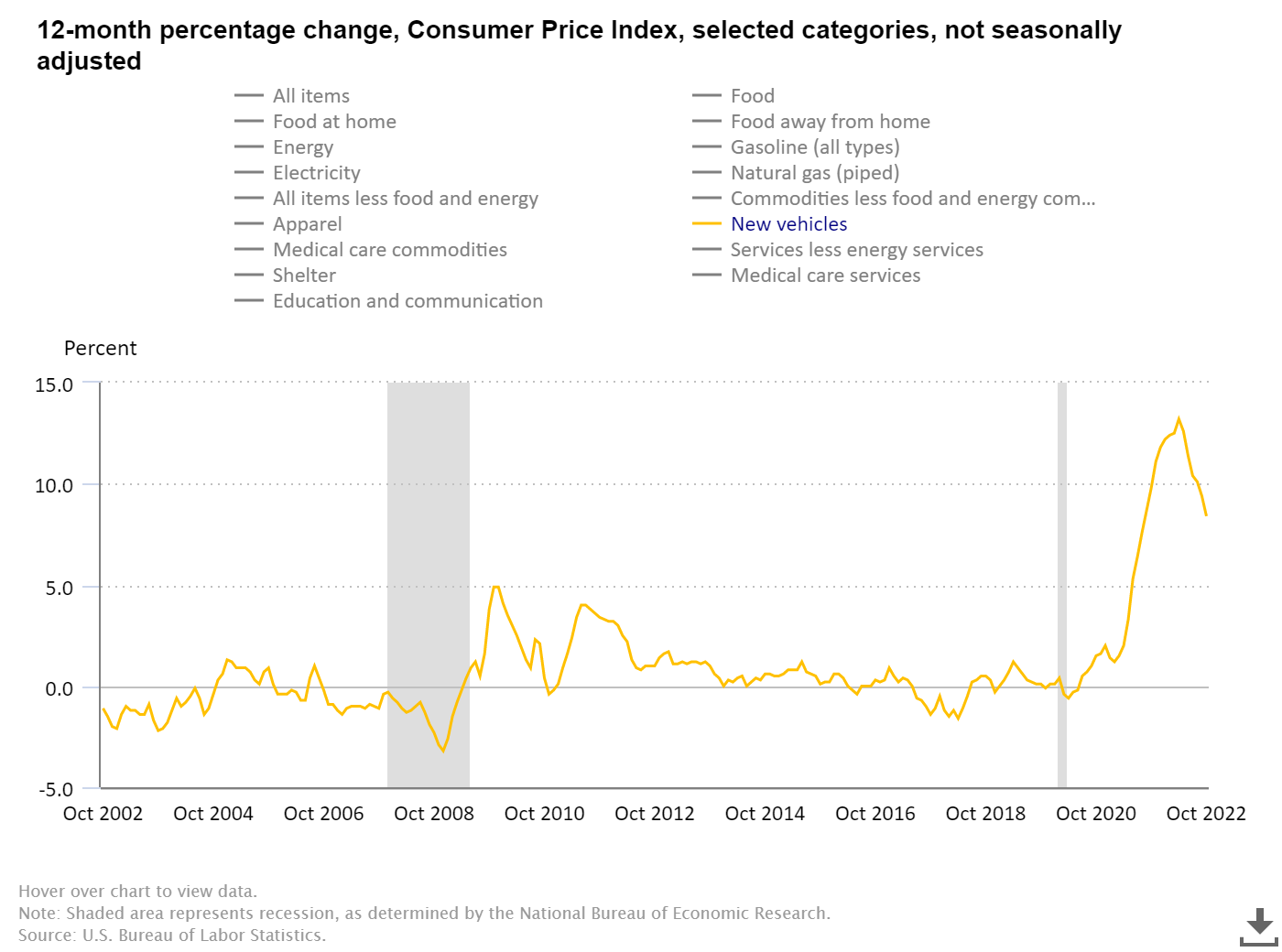

Today’s consumer price index report also shows that the new car price index, which had a parabola during the pandemic, is also falling. Again, the best way to deal with inflation is to increase supply in the market.

So does this data represent a tipping point? Have you seen the peak growth rate of inflation?

I will say this on this topic. At this point last year, growth in many inflation data was still on the rise and, above all, Russia’s invasion of Ukraine in February. Since then, there have been major rate hikes within the system by the Fed, the biggest driver of core inflation in America, which he expects to cool in 2023. These facts are here today where they were not in November 2021.

But the Federal Reserve is feeling pressure to trigger an unemployment recession to bring inflation data back to 2%.

In my sixth and final recession warning on August 5th, I wrote about two ways you can avoid a nasty unemployment recession. Here are 2 things I’m looking for:

1. rate goes down To put the housing sector back together.

Even if mortgage rates drop toward 5%, you can still stabilize your home if you have time. Traditionally, housing demand rises when mortgage rates fall below 4%. We need to stop the bleeding and what we’ve seen in the data is that buyers entered the housing market when interest rates went back to 5%.

However, the 5% interest rate did not last long as the Federal Reserve decided that this was counterproductive to creating an unemployment recession. To get the housing market out of recession, we need to see lower interest rates and keep them there for a while.

2. Inflation falls, the Fed stops rate hikes and reverses course, similar to 2018.

Some inflation data are already cooling and will be reflected in the data lines. However, rent inflation will not be lower in the data until 2023.

All six of my recession flags are up, so I’m keeping an eye on the unemployment claims data that rose today. The badger labor market is holding up.

So for today this is a small win, but it will take many more months to transform this economy.

[ad_2]

Source link