[ad_1]

More than 30 years ago, Australia’s then prime minister, Paul Keating, told parliament, “For the first time in our history… ordinary Australians will be able to build decent nest eggs for retirement.” It will be,” he said, announcing the introduction of a compulsory retirement pension system. .

As Keating emphasized at the time, the main purpose of superannuation over the next 30 years was to help Australians live after retirement. The Super Guarantee is designed to accumulate in two ways. One is an investment that will compound over time, and the other is to ensure that the investment remains pristine until retirement, giving it adequate accumulation opportunities.

As a result, it is not surprising that there are only very specific circumstances in which you can receive your retirement pension before you have finished your job.

Related: How do I find the unique identifier for my retirement annuity?

When can I withdraw from Super?

There are some conditions for early access to superannuation, but most Australians will only get access to superannuation if they meet the conditions for release if:

- You reach the age of preservation and retire.Also

- Reaching Conservation Age and Starting the Transition to a Retirement Pension.Also

- you will be 65 years old.

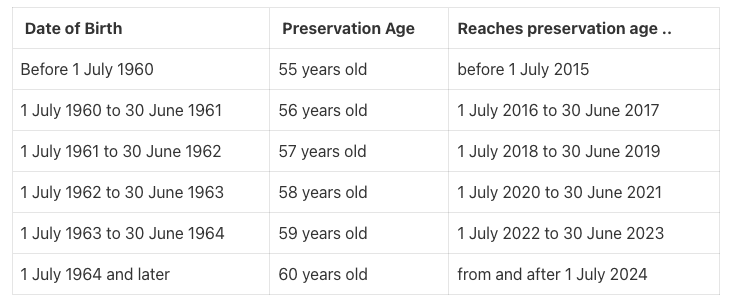

Your save age depends on when you were born, according to the table below.

Most importantly, the storage age is not the same as the age at which you can access your old-age pension (66 years and 6 months until you turn 67 on July 1, 2023). So if she chooses to retire at age 60, she should be able to self-finance that retirement at least until age 67.

With the increasing longevity in recent years, the eligibility age for old-age pensions has been raised. Successive federal governments have also become increasingly concerned about the cost of funding old-age pensions among Australia’s growing cohort of older adults.

Super early release

There are some extenuating circumstances in which you can receive your retirement pension early. These fall into five main areas: severe financial hardship, compassionate reasons, terminal illness, permanently physically or mentally incapacitated, or temporarily incapacitated.

For more information on the early release of your retirement annuity, check out our guide.

Retirement pension withdrawal during Covid

Eligible Australians experiencing Covid-19 hardships between April and December 2020 will have access to up to $10,000 in Super during the 2019-2020 financial year, July 1, 2020 An additional $10,000 was available between 1st and 31st December 2020.

super lump sum payment

Once you have reached the age of protection and meet the conditions for release, you can withdraw your retirement pension as a lump sum or as a source of income. If you want to withdraw in bulk, check if the superannuation fund allows it (most large funds do).

You will then need to either contact the fund directly or locate the “Apply for Payment” form on the fund’s website and complete and verify it. You can withdraw part of your annuity in full or in full. Please note that withdrawing all of your Superannuation will permanently close your account and you will lose any insurance benefits your account was provided with.

supermarket as a source of income

Another option is to use your current superannuation fund (or any superannuation fund) and convert your superannuation to an account-based annuity. This can be done online for existing funds. It can also be done using an application form for new fund account-based pensions.

You must specify the frequency and amount of payments. If you do not want to lose your pension tax exempt status, there is a minimum annual pension withdrawal rate.

Minimum annual withdrawal rates currently range from 2% to 7% of balance depending on age, but will return to pre-corona levels of 4% to 14% in fiscal year 2023/2024.

Partial retirement?

You can access the Transition to Retirement Pension (also known as Income Stream or TRIS) if you have reached the Conservation Age. This allows you to continue working part-time while maintaining income consistent with your previous full-time income.

To do this, transfer part of the superannuation to an account-based annuity using the superannuation fund. This type of income stream cannot be transferred in bulk.

How much tax will you have to pay when you withdraw your retirement allowance?

If you retire over the age of 60 and participate in a taxable fund (which is the case with most superannuation funds), you do not have to pay tax on your lump sum withdrawal. If you are over 60, there is also zero tax on income earned from account-based pensions.

However, if the retention age is less than 60, some taxes may apply depending on whether the fund is already taxed within the fund and how much it exceeds the low tax rate threshold (currently $215,000). You may have to pay. It is withdrawn.

These can be very complex calculations and the ATO has detailed explanations.

Frequently Asked Questions

What is the minimum withdrawal amount for retirement?

There is no actual minimum lump sum withdrawal amount if you retire and reach the retention age. However, there is a minimum annual pension amount that must be paid depending on age.

Can I withdraw my Super to pay off my debt?

What is the withdrawal age for retirement benefits?

What are the rules for removing retirement allowances when transferred overseas?

How much Super can you withdraw?

[ad_2]

Source link