[ad_1]

winning horse

investment paper

Fujifilm (OTCPK:FUJIF) has experienced disappointing results in terms of vaccine supply as Novavax was expected to be a game changer. Nonetheless, the company’s forecast for the fiscal year ending March 31, 2023 has been revised upwards due to strong sales at the moment.we believe in sharing Price Correction YTD is an opportunity to buy shares.

quick primer

Founded in 1934, Fujifilm is a fine chemical manufacturer spun out from Daicel (OTCPK: DACHF), which manufactured photographic film. As a manufacturer of diagnostic imaging systems such as endoscopes, CTs, MRIs, and X-ray scanners, we are focusing on expanding as a contract development and manufacturing organization, and have also expanded into the healthcare field.

The company also offers materials such as photoresists and optical films for the semiconductor industry, business process outsourcing (digitalization of printing and content management as an alternative to office equipment), and pharmaceuticals. At first glance, the company appears to have diverse and different business models, but the central themes are Fujifilm’s technical expertise in imaging and manufacturing skills (high quality control and production yield improvement). etc.) to relevant new markets.

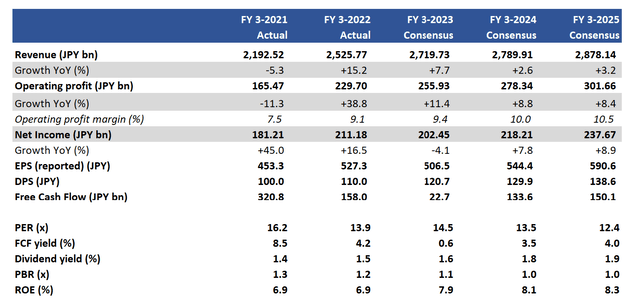

Key financial information with consensus forecasts

Key financial information, including consensus forecasts (company, Refinitiv)

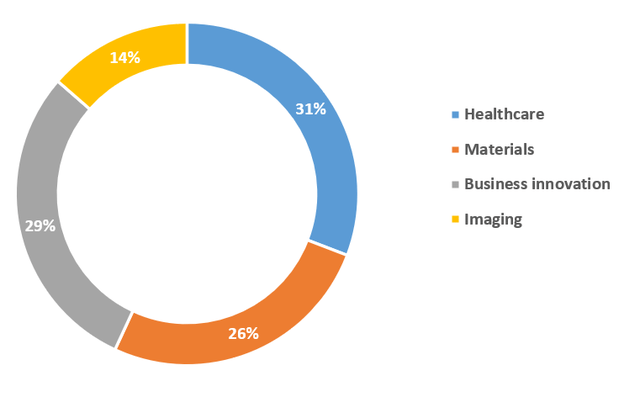

Net sales ratio by business segment in the 1st and 2nd quarters of FY3/23

Sales ratio by business segment in Q1-2 of FY3/23 (company)

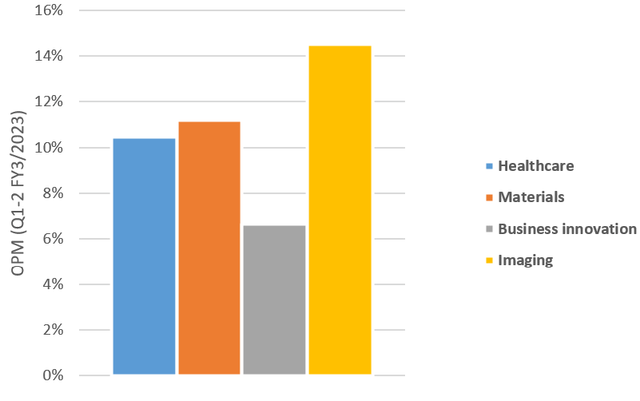

Operating profit margin by business segment in 1st and 2nd quarters of FY3/23

Q1-2 Operating profit margin by business segment for FY03/23 (company)

our goal

Given our bullish stance in March 2021 when the outlook for the healthcare business, especially the CDMO business, looked positive, we want to revisit our initial outlook. Unfortunately, Novavax’s (NVAX) supply deal with Fujifilm has ended due to low demand for his COVID-19 vaccine. Novavax has agreed to pay up to $185 million in settlement payments.

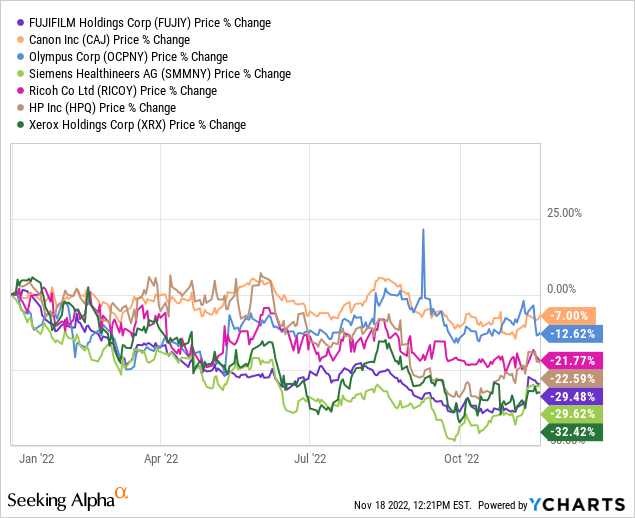

Fujifilm’s shares underperformed their imaging and office services peers as Canon (CAJ) and Olympus (OTCPK:OCPNY) held up, largely benefiting from a weaker yen.

Novavax issues were expected

It’s a shame the company wasn’t able to leverage their relationship with Novavax. There has been a clear lack of positive news flow since the initial announcement in July 2020, making it more evident that his uptake of COVID-19 meds in the US has been delayed and ultimately too low. became. Thankfully, the payment of the settlement money started from the second quarter of the fiscal year ending March 2023.

Despite this backlash, the Company’s results in the first and second quarters of FY3/23 were solid, and both net sales and operating income increased 12% YoY. Operating profit hit a record high for the second quarter of the fiscal year ending March 2023, and the company raised its full-year operating profit guidance to his record high of ¥260 billion/US$1.8 billion. This was a positive surprise as the company was in a position to meet its medium-term financial targets one year ahead of schedule.

There are two sources of current revenue. Imaging is the largest contributor, driven by both consumer and professional product demand. Fujifilm has been an innovative player in the smartphone printer market with hits like the Instax Mini Link 2. For professionals, the new mirrorless camera HS2 released in July 2022 has been well received. Another smaller driver is business innovation, consisting of demand for MFPs and printers as office workers return, and business process outsourcing services. Overall, Imaging is expected to be the main driver of year-over-year growth in the year ending March 2023.

long term outlook

Despite its experience with Novavax, the company continues to invest in expanding the capabilities of its contract development and manufacturing organization business at new facilities in Japan. Strategically, we believe that demand for biopharmaceuticals and vaccines will increase in Japan and Asia, reducing our dependence on overseas suppliers. He believes that the start of operations at the new Toyama base will not take place until the fiscal year ending March 2027, but that business expansion will be a plus in the long term.

Other strategic initiatives include investment in a new CMP (chemical-mechanical polishing) slurry plant in Kumamoto, Japan, which is scheduled to start operations in January 2024. Such as post-CMP cleaners and photoresist materials.

There is no guarantee that these investments will yield high returns, but the company’s recent ROIC trend is encouraging, rising from 3.5% in FY03/13 to 7.0% in FY03/22. Absolute levels remain relatively low, but indicate the company is improving its capital allocation to more profitable investments.

evaluation

Consensus projections (see key financial table above) show the stock trading at 13.5 times earnings in FY03/24, with a free cash flow yield of 3.5%. These indicators look attractive. Especially given the company’s growing healthcare-related exposures, which typically impose a high valuation premium.

risk

Upside risks stem from a seasonal spike in demand for video products in H2-FY03/23, resulting in better-than-expected earnings and significantly overshooting revised guidance. The easing of lockdowns in China will boost sales of medical and office equipment, helping to revive earnings in the region.

The current forecast for the dollar/yen exchange rate in FY3/23 is ¥135, and there is downside risk due to yen appreciation. A significant increase in silver prices will negatively affect the profitability of photographic film.

Conclusion

Fujifilm is gradually transforming its business portfolio into a highly profitable one. While the company is unlikely to exhibit a high growth profile, it does show signs of an attractive compounding business. The Novavax episode is disappointing, but the company was able to grow revenue to record levels last quarter. With the YTD stock correction, we believe this is a buying opportunity.

[ad_2]

Source link