[ad_1]

Starting this week, every Monday, the Housing Market Tracker article will analyze weekly data to provide an update on the U.S. housing market and economy. This weekly tracker gives you up-to-date information on your data line without having to wait for your monthly housing data report.

The housing market is one of those sectors that can turn positive or negative very quickly, depending on mortgage rates and temporary shocks like we saw with COVID-19. This weekly update reminds you not to be surprised by the changes. It also points out what to watch out for during the week.

The three categories covered here are weekly purchase application data. Altos Research Weekly inventory data, and recent bond market/mortgage rate trends. Unlike sales and pricing data, which takes 30 days to report, this housing market tracker updates data lines released weekly.

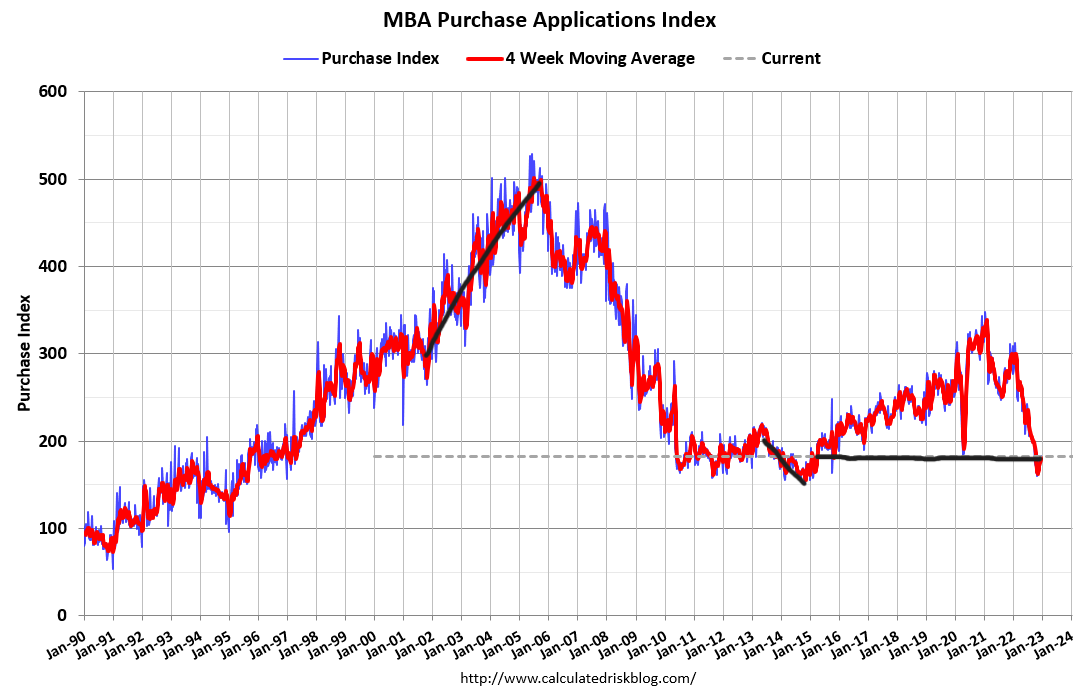

Purchasing application data

Requisition data is a future line of data that should account for sales data 30-90 days ahead. This has been key research data for me for the last 11 years. Mortgage primary buyers are the driving force behind the US housing market, and when this data declines or rises, so does housing.

The positive trend in purchase requisition data that began in November following the first weaker-than-expected CPI inflation report last week continues. Mortgage rates he began to fall in November, and purchase requisition data, which showed a sharp drop in demand, has finally stabilized and bounced back from its lows.

Weekly decline in apps purchased was modest 0.1%The year-on-year decrease is . 36% However, the peak of the decline is 46% Year-over-year, we bounced off the lows in a notable fashion.

This is the stable period for this data line. For this trend to be more valuable, it needs to last 14-18 weeks. The outflow of purchase requisition data has stopped. As long as the year-on-year decline tapers off, that’s good for the housing market.

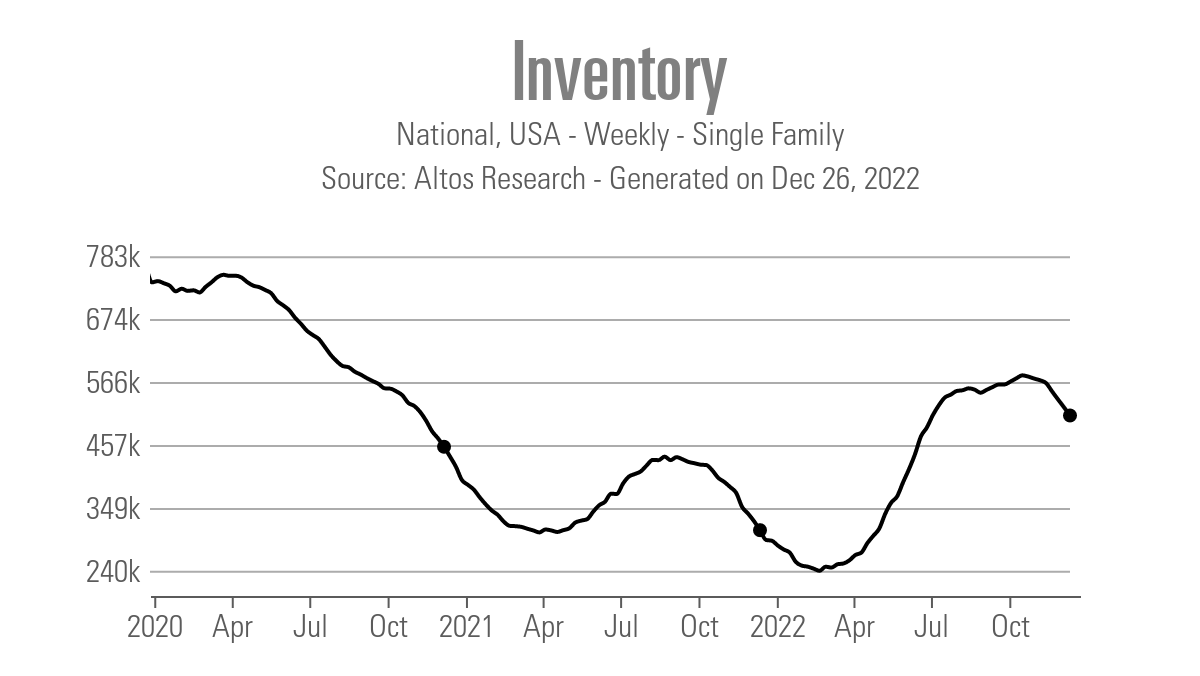

housing market inventory

Altos Research data shows that weekly inventory 521,957 to 507,934 last week. This is for single family homes only. For more on this data his line, check out the Top of Mind weekly podcast hosted by Altos Research founder Mike Simonsen.

One of my beliefs is that if demand weakens over the long term, housing inventory could continue to rise. The last time this happened he was in 2014. At that time, purchase requisition data for that year went negative, similar to what we saw in 2022.

Traditionally, stocks decrease in the fall and winter and increase in the spring and summer. Currently, inventories are declining as usual, but purchase requisition data started increasing seven weeks before him. I look at requisition data as an indicator of demand 30-90 days ahead. Purchase requisition data began to rise 7 weeks ago and we expect 30 to 90 days from now, so part of this decline in inventory is due to increased demand, not just the seasonal decline we’re seeing right now. .

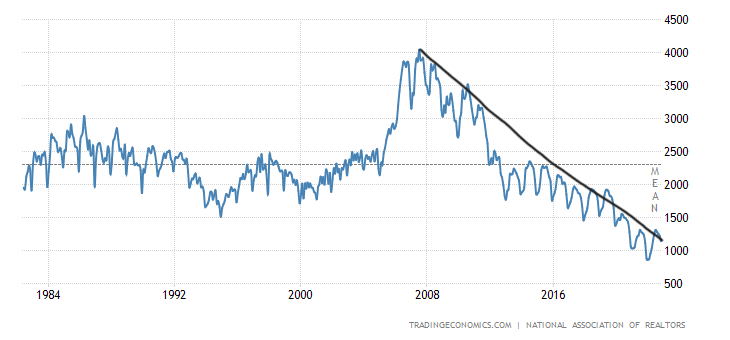

of National Real Estate AssociationMonthly inventory data is displayed monthly along with existing home sales reports. This, like all existing home sales reports, is a thing of the past.NAR inventory data has been declining over the past four months and is now 1.14 millionWe are on the verge of collapse One million Again, with mortgage rates going up this year, I didn’t expect this to happen, but it looks like it will happen within the next two months.In some circumstances, the all-time low for this data line is 860,000 January 2022.

Bond Market and Mortgage Rates

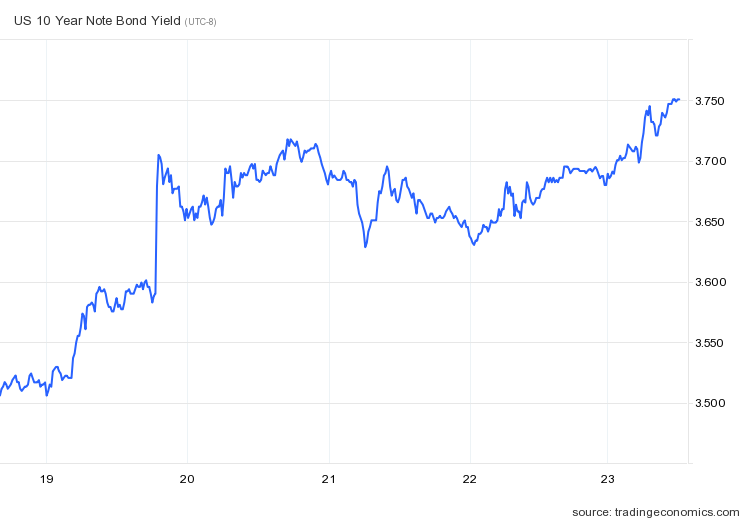

10-year yields weren’t doing well last week. Bond yields rose positively despite weak PCE data for him last week.Notice from Bank of Japan sent shockwaves around the world and bond yields rose earlier in the week.

On the other hand, mortgage interest rates 1% Below recent highs and up 0.19% From the bottom to the basis point that occurred on December 15th 6.32% Today, December 26th. With deals involving buydowns and seller credits, the interest rates some home buyers are getting are lower than the headlines you see every day. But it’s been a lousy week for mortgage rates.

As far as housing market economic reports are concerned, FHFAMore Home Price Index and S&P CoreLogic house prices in case shiller This week’s index.waiting at home With sales coming up Wednesday, I doubt this report fully captures the last seven weeks of push in mortgage application data.

Also, there are some regions Federal Reserve Bank Terrible manufacturing data these days and very important unemployment claims data every Thursday. It’s a week with shortened holidays and the market opens the following week.

There were 2 positives and 1 negative in the weekly data. I’ve run out of purchase requisition data. To call it a real trend, this kind of action she wants to last 14-18 weeks.The bottoming out of the data line is that mortgage rates Five%.

Weekly housing inventories are declining, as is typical for this time of year, partly due to increased demand. However, unlike the beginning of 2022, we won’t be entering the year with his 3%, an all-time low for inventory and mortgage rates. The housing market was unhealthy at the time, and by February 2022, as the bidding wars escalated in January, February, and March until mortgage rates began to rise, I coined savagely unhealthy phrases. I was.

The Fed has more days in the market each year, so more balances need to be seen. I’m not a fan of the housing market where my days on the market are at the level of teenagers. This tends to mean there aren’t enough commodities to meet market demand, which could push prices so high that the Fed calls for housing adjustments.

Sure, it’s been a crazy year. The year started with too many bidding wars, followed by a significant interest rate hike, which had a big impact on demand, but towards the end of the year interest rates fell and future data showed more stability. I’m here.

Every Monday, I feed this weekly housing market tracker with the latest weekly data and get all the housing data one day at a time to understand this market.

[ad_2]

Source link