[ad_1]

JHVEPhoto/iStock Editorial via Getty Images

prologue

In the aftermath of its fourth-quarter report, Intel’s (NASDAQ: INTC) stocks are crashing. The semiconductor industry is battling a challenging macro environment. However, Intel’s Q4 2022 financial performance and his Q1 2023 forward guidance are a total nightmare.For me, Intel is still multi-year A play of national importance, and I view this recent quarter as one of the bumps we expect to see on the road to glory.

- Inter: Preparing for bumpy glory [25th October 2021]

Despite bringing a technologist named Pat Gelsinger to the CEO position almost two years ago, Intel’s performance shows no signs of improving (in any case). As you may know, Intel is entering a hefty investment cycle as the once formidable semiconductor giant works towards his Gelsinger’s “IDM 2.0” strategy. Pat has repeatedly talked about his Intel big guys.The company continues to lose market share. That said, Intel has an interesting product and process roadmap (5 process nodes in 4 years), When If Intel shareholders could well be rewarded if Pat & Co. does well in the next few years.

In this article, we share Intel’s fourth quarter analysis and provide the latest assessment of the company. Additionally, review Intel’s technical charts and quant factor grades to make informed investment decisions.

Intel Quarterly Breakdown

A semiconductor chip shortage in 2020-2021 has turned into a chip glut in an uncertain macroeconomic environment. Despite entering the quarter with significantly lower estimates, Intel managed to miss analyst estimates by about $500 million. The company blamed industry-wide demand challenges and competitive pressures for this loss of revenue.

Adding to this misery, Intel’s gross margin continued to deteriorate, to ~43.8% (down 1210 bps year-on-year). As a result of weaker earnings and margins, Intel’s EPS plunged to his $0.10 (down 92% year-over-year), well below his $0.20 guidance.

Intel Q4 2022 Earnings Release

From a revenue standpoint, Intel had a terrible quarter. That said, Intel generated $7.7 billion in operating cash and $3.1 billion in free cash flow in the fourth quarter. From this free cash flow, the company paid out his $1.5 billion dividend. Let’s dive deep into the performance of each of Intel’s business segments to truly understand the fundamental underlying trends.

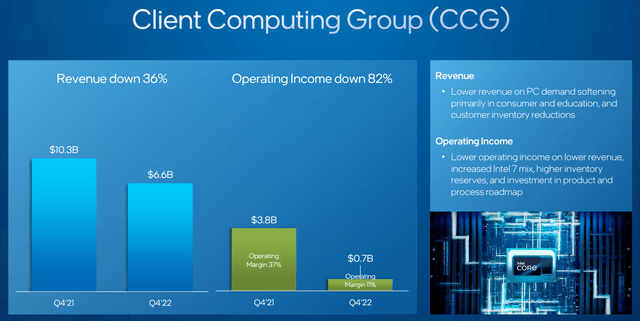

Intel’s Client Computing Group revenue in the fourth quarter was $6.6 billion, down 36% year-over-year. After a massive increase in demand for hybrid work in 2020-2021, the PC market has slowed significantly and Intel’s CCG business is currently taking a big hit. Due to high channel inventory, Intel is severely short of shipments. The normalization of demand in this segment is set to continue for several more quarters. Therefore, Intel’s CCG business may continue to come under pressure for the foreseeable future.

Intel’s weak result could point to a further loss of market share against AMD (AMD), but we’ll find out more about that when AMD reports in today’s after-hours session. As shown, Intel’s CCG business is experiencing negative operating leverage, and we expect this margin pressure to continue as long as spending on Intel’s product and process roadmap remains high.

Intel Q4 2022 Earnings Release

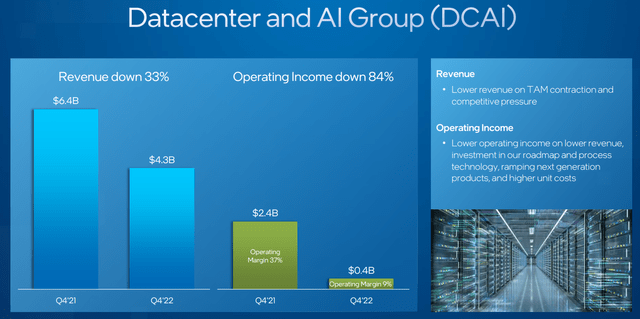

After reporting disappointing numbers in the third quarter, Intel’s Data Center and AI Group revenue fell about 33% year-over-year in the fourth quarter, but increased 2.4% quarter-on-quarter. Part of the weakness is due to the shrinking market, but I think rivals like AMD and Nvidia (NVDA) are dominating Intel in the data center market. The launch of Sapphire Rapids should help Intel. But the semiconductor giant is really cutting jobs in this important market as its competitors innovate faster than Intel.

Intel Q4 2022 Earnings Release

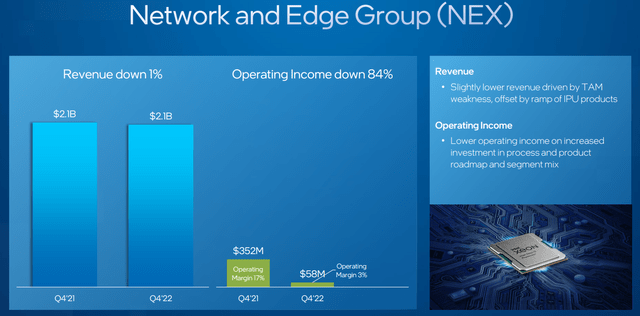

In the fourth quarter, Intel’s network and edge group revenues were down just 1% year-over-year. IPU product growth largely offset revenue declines from TAM contraction. Like other lines of business, Intel’s NEX segment had weak operating margins.

Intel Q4 2022 Earnings Release

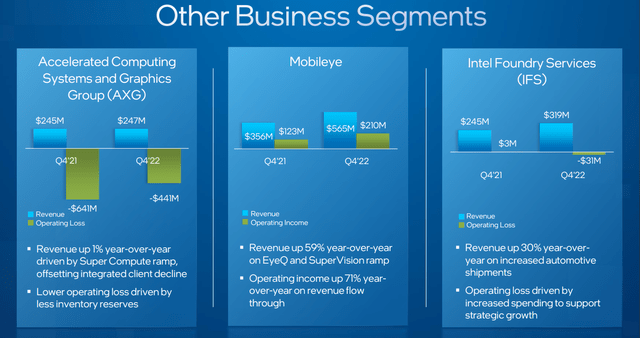

Mobileye is now publicly traded as an independent company, but Intel still owns approximately 94% of Mobileye. And this is probably the only bright spot in Intel’s entire Q4 report. Mobileye’s revenue increased 59% year-over-year and operating profit increased 71% year-over-year. The self-driving car market may not mature in a few years. However, Mobileye has the potential to create significant shareholder value for Intel investors!

Intel Q4 2022 Earnings Release

Intel’s guidance is an absolute nightmare

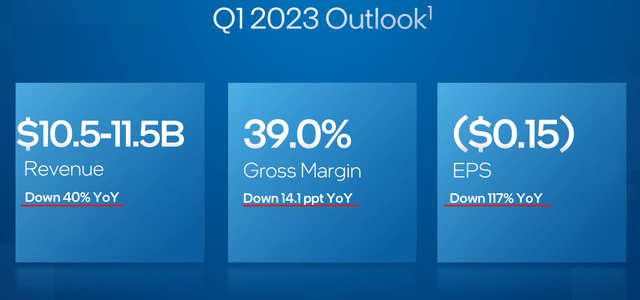

For the first quarter of 2023, Intel management provided yet another kitchen sink-like guidance. That’s $10.5 billion to $11.5 billion in revenue (down 40% year-over-year), 39% gross margin (down ~480 bps consecutively), and minus $0.15 EPS!

Intel Q4 2022 Earnings Release

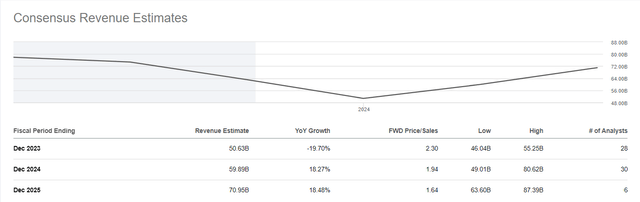

Despite Intel’s poor Q4 results, its guidance for Q1 2023 is downright ugly! The macroeconomic backdrop is likely to remain challenging, with analyst estimates for Annual revenue is expected to drop to $50 billion.

Seeking Alpha

Seeking Alpha

Demand pressure should start to ease in the second half of 2023, according to Intel management, and the long-term TAM opportunity remains enormous. According to Pat Gelsinger, Intel’s total addressable market could double in the next decade.

Digitalization, all accelerated by the four superpowers of AI, pervasive connectivity, cloud-to-edge infrastructure, and ubiquitous computing, is driving a sustained need for more semiconductors, with the market expected to reach 2030. It is expected to double to $1 trillion by 2020.

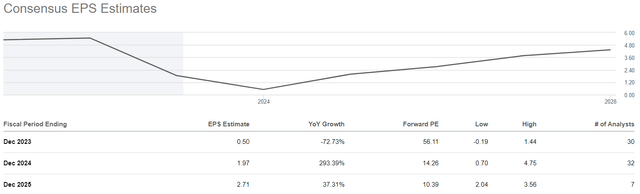

Semiconductor growth is inevitable, so Intel’s IDM 2.0 is a worthy long-term bet right now. There is a big question mark on Intel’s ability to execute, but I think Intel’s growth forecast of 10-12% CAGR over the next 4-5 years is achievable. [post a reset in 2023]If Intel can hit those double-digit revenue growth targets and get gross margins back in the 55-60% range after 2023, I think it’s a tipping point for Intel this decade.

Gelsinger’s hybrid sourcing strategy should enable Intel to offer competitive semiconductors in the next few years, but the use of external foundries such as TSMC (TSM) may continue to squeeze Intel’s margins. I have. In addition, Intel’s future revenue growth efforts are based on expanding its costly foundry business. If Intel fails to hit his 5-node target in 4 years, it could end up falling behind the competition and even more technically behind!With all this in mind, Intel’s Build a conservative rating model.

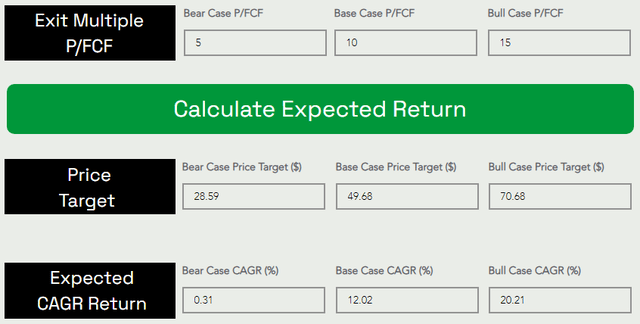

Intel’s fair value and expected return

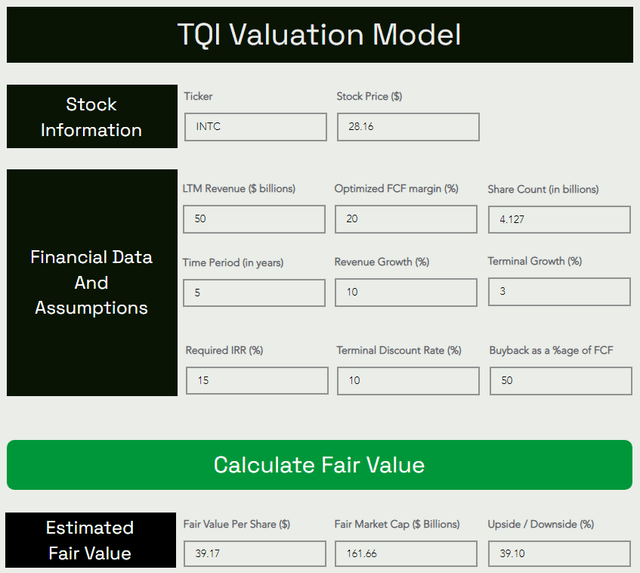

To account for the ongoing reset in Intel’s business, we assumed a revenue base of $50 billion (estimated in 2023) when building our valuation model for the company. The remaining assumptions are simple. However, if you have any questions, let us know in the comments section below.

TQI rating model (TQIG.org)

TQI rating model (TQIG.org)

Based on these results, if you buy Intel at its current price of $28 and hold the stock for 5 years, you can expect a CAGR return of up to 12%. These returns are higher than TQI’s Buyback Dividend Portfolio hurdle rate (10%), so we still like Intel from a valuation perspective.

INTC Technical Charts and Quant Factor Grades Review

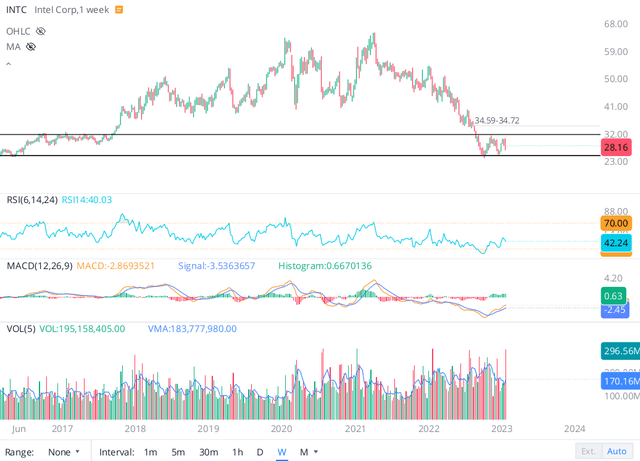

After suffering a devastating 2021-2022 decline, Intel’s stock appears to be forming a Stage 1 base in the $24-$32 range from September 2022 onwards.

WeBull Desktop

Technically, Intel’s stock was recently rejected from the top end of this base and a retest for the bottom end of the base could happen soon. In the event of a severe recession, Intel could decline. However, if you get a soft or soft landing, the downside is probably limited to $24.

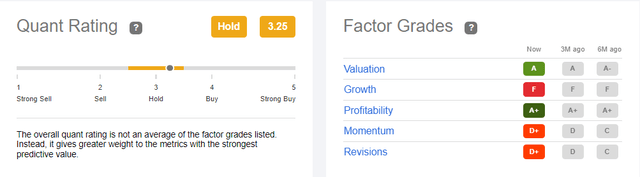

SeekingAlpha Quant Rating

According to SA’s quant rating system, Intel is rated 3.25/5, with high valuation (“A”) and profitability (“A+”) grades, growth (“F”) and momentum (“D+”) grades. offset by lower grades. , and revision (“D+”). In my view, Intel’s profitability grade is set to deteriorate over the next few quarters as earnings turn negative in 2023, and any negative or depressed earnings will also lower Intel’s relative valuation. . So, I think Intel’s quant factor grades will move from ‘Hold’ to ‘Sell’ ratings in the next 6-12 months.this is the reason I don’t like buying Intel anytime soon.

Intel’s dividend isn’t under serious threat right now, but that could change soon

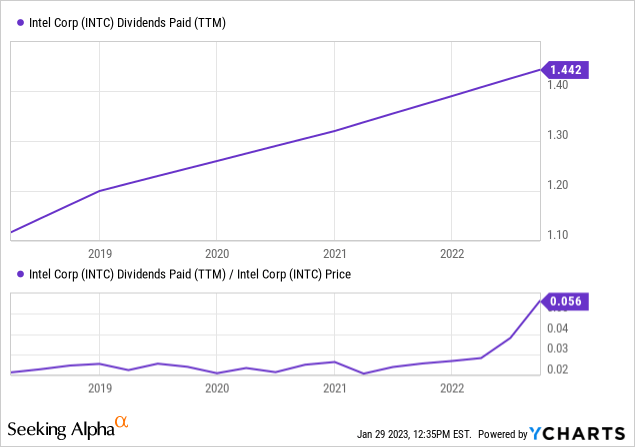

Intel’s dividend yield surged to 5.6% as the stock price plummeted in 2022. Intel’s dividend yield looks attractive, but sharp increases in dividend yields generally represent increased risk of dividend cuts.

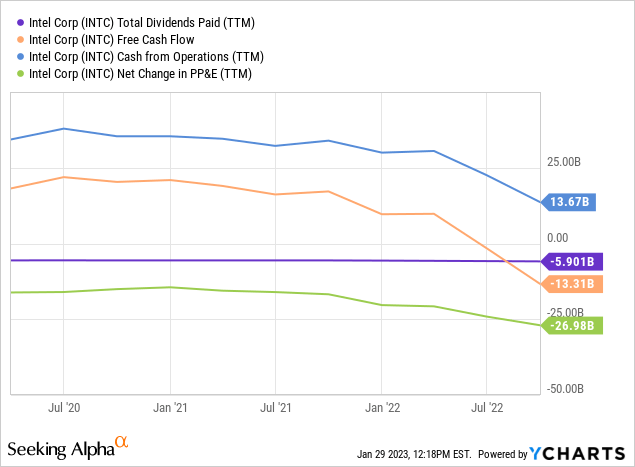

As you know, Intel has had a heavy CAPEX spending cycle with about $27 billion spent on PP&E in the last 12 months. During this transition period, Intel experienced a complex cash burn situation as revenues, margins and operating cash flow declined sharply.

In the fourth quarter, Intel generated positive FCF of $3.1 billion and paid a dividend of $1.5 billion. However, in the last 12 months, Intel has reported negative free cash flow of -$13.3 billion, and according to management’s latest commentary, Intel will also report negative free cash flow for the first half of 2023. I plan to report it.

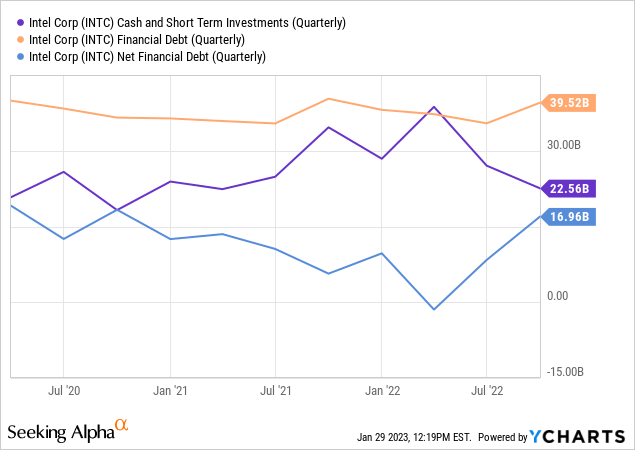

As you can see from the chart above, Intel’s financial debt is increasing, its cash position is declining, and its net financial debt is skyrocketing. Given the uncertain macroeconomic environment and Intel’s ongoing investment cycle, management could be forced to cut his dividend in the second half of 2023 (especially if a recession hits). So if you’re looking to buy intel just to get a dividend, I suggest looking elsewhere.

in conclusion

Despite the apparent deterioration in financial performance, Intel remains a company of national importance as the Western Hemisphere’s only large semiconductor manufacturer. Given the uncertain macroeconomic environment, Intel’s financial performance could remain fluid for his 2023. But based on future valuations, Intel looks like a decent buy at current levels.

Intel’s stock price forms a base in the $24-$32 range. I prefer to shop towards the bottom of this range, but $28 is fine to get in here. Based on a combination of fundamental, quantitative, and technical analysis, I think Intel is a conservative long-term investment at current levels. And I strongly prefer the slow, staggered accumulation on this counter. If you’re looking at Intel as a short-term purchase, or as a way to earn dividends in the short to medium term, we encourage you to look elsewhere!

Key takeaway: I rate Intel as a medium long term BUY at $28.

Thanks for reading and happy investment. Share your thoughts, concerns, and/or questions in the comments section below.

[ad_2]

Source link