[ad_1]

olemedia

established theory

Prices are finally back on the side of investors as the cybersecurity industry continues to decline along with the technology sector as a whole.Palo Alto Networks, Inc. (Nasdaq: PANW) leading position in the cybersecurity industry and its diversified portfolio Next-generation solutions and products, coupled with undervalued fundamentals, create a compelling case for investors. However, it makes sense to consider a more diverse approach. First Trust Nasdaq CEA Cybersecurity ETF (NASDAQ: CIBR) offers the opportunity to invest across industries at relatively low fees.

Therefore, this article discusses whether CIBR can offer investors more value than Palo Alto Networks.

Why CIBR?

The First Trust Nasdaq CEA Cybersecurity ETF is the largest in terms of funds under management. CIBR has a fairly high management fee of 0.6% and a portfolio of 37 stocks. The three largest holdings are Infosys (INFY), Cisco (CSCO), and Broadcom (AVGO).

The idea of using the fund’s rather narrow portfolio to capitalize on the rapid growth of the market, as most of CIBR’s companies are absolute leaders in their field, separated from their competitors by groundbreaking products. is.

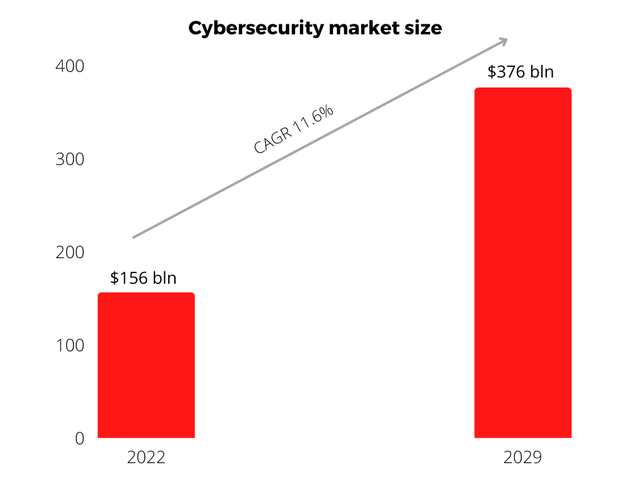

Over the next few years, the key growth driver for the industry will be strong demand for network security solutions to protect cloud applications and IoT-enabled devices. In today’s reality, ensuring cybersecurity is becoming one of the main tasks of any business. The need and importance of cybersecurity is recognized at all levels. For example, industrial companies are reducing the use of human labor in production and betting heavily on automation. Therefore, there is a great need for software to ensure the safety of production processes where IoT-connected devices play a vital role. Overall, Fortune Business Insights predicts that the global cybersecurity market could grow to $376 billion by 2029.

Fortune Business Insight

I believe CIBR is the best cybersecurity ETF as it has over $4.5 billion in assets under management (“AUM”) and a balanced portfolio of large and large companies in various sectors. increase. In a previous article, we compared it to its leading peer, First Trust Nasdaq CEA Cybersecurity ETF (HACK).

Palo Alto case

The company operates in three segments: network security, cloud security, and SOC security.

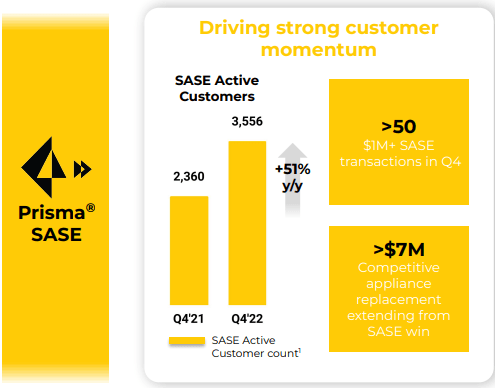

In the network security segment, Palo Alto offers the complete network security system Prisma SASE program. It allows companies to control inbound and outbound traffic and protect internal networks from external cyberattacks. Prisma SASE is a set product that can be purchased individually or separately. 74% of Global 2000 companies were Prisma SASE customers at the end of 2021. The total number of active customers reached 3,556 in FQ4.

Palo Alto

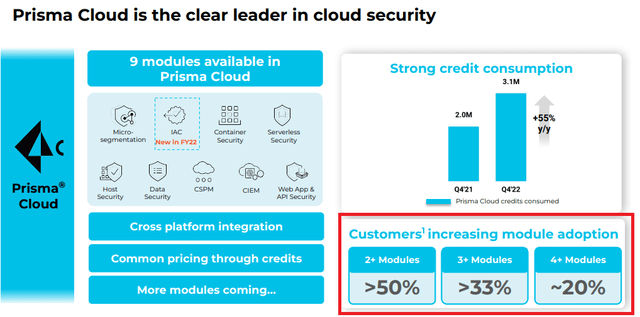

In the cloud segment, the company’s flagship product is the Prisma CLOUD program. Prisma CLOUD is an industry-leading cloud-based security platform that provides end-to-end protection for hosts, containers, and serverless computing throughout the application lifecycle. You can monitor the performance of every application running in the cloud, every device entering the cloud, your data center, and your entire cloud infrastructure. Module adoption is on the rise as more than half of our customers are currently using two or more modules. The program processes his 700 billion events on threats around the world each week.

Palo Alto

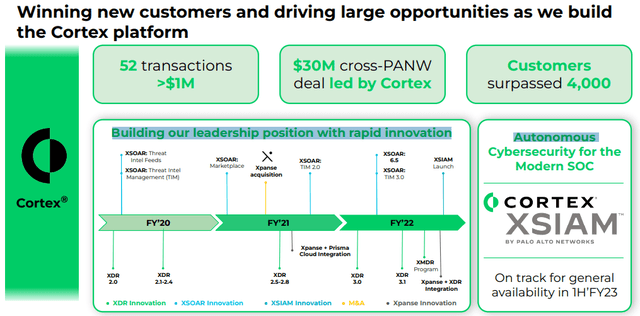

According to Forrester, the average security operations team receives over 11,000 security alerts daily, 28% of which are never addressed, and each incident takes an average of four days or more to investigate.

With the CORTEX XDR program, Palo Alto aims to detect and neutralize 100% of threats, allowing incidents to be handled and analyzed in minutes. Cortex is based on artificial intelligence and machine learning technology and can automate most tasks. Therefore, the reliance on the human factor is reduced.

Palo Alto

A key factor is that by combining all three Palo Alto solutions, enterprises can build effective next-generation cybersecurity systems based on a Zero Trust security model. Corporate resources without exception.

There is no alternative on the market that can build a complete Zero Trust system. As such, Palo Alto has a wide moat to defend against competitors.

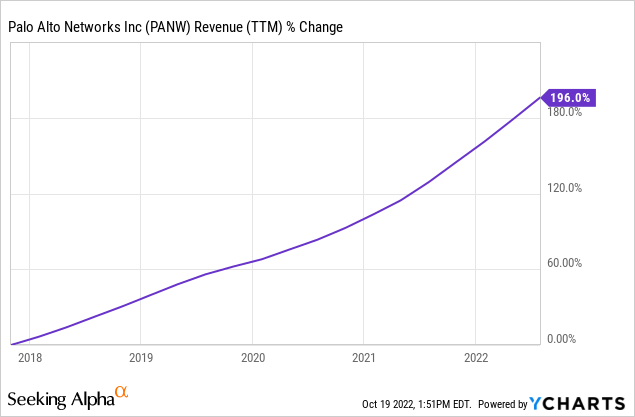

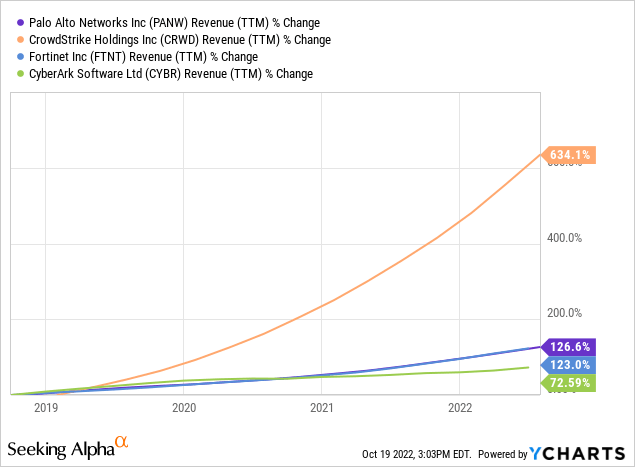

Palo Alto Maintains High Growth, But It’s Not Enough

Over the past five years, the company’s revenue CAGR was 19.3% and its share price CAGR was 26.4%.

At the same time, Palo Alto maintains stable positive free cash flow.

However, other industry leaders are seeing the same trend.

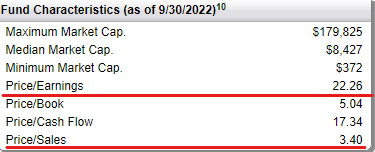

In terms of valuation, Palo Alto’s P/S is almost double the fund’s, so it’s not cheaper than CIBR.

first trust

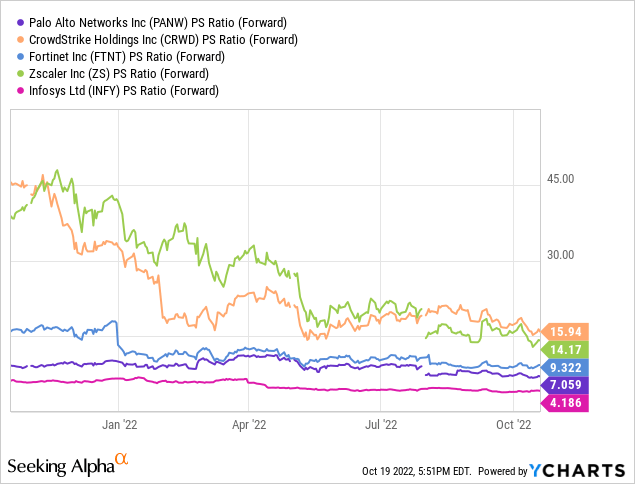

That’s because Palo Alto’s growth rate is higher than most companies in the ETF. PANW looks pretty cheap compared to other big, fast-growing companies.

Palo Alto has a fairly wide moat in the form of a full-fledged Zero Trust system and currently has no alternatives. The risks here are much higher than with CIBR. The moat is probably wider than most of its competitors, but not strong enough to warrant long-term organic growth. The industry still has no clear leader, and different companies occupy different niches.

Conclusion

Palo Alto is primarily betting on the continued global growth of the cybersecurity market and surging demand for Zero Trust products. The company looks promising and growing rapidly. This may be true, but I prefer CIBR. It has a quality portfolio of excellent companies that are smartly rebalanced fairly often.

PANW will surely recover in the rest of the market, but CIBR looks like the safer option to me.

[ad_2]

Source link