[ad_1]

Borrowers with high credit scores can potentially save thousands of dollars by consolidating their credit card debt into a new loan. (iStock)

Minimizing high interest credit card debt is an expensive way to pay off your balance. Credit card interest accrues daily and adds to the total cost of paying off your debt over time.

One popular way to consolidate credit card debt is with a personal loan. This is a type of lump sum unsecured loan that is repaid in fixed monthly installments at a low interest rate. And with interest rates on personal loans lower than ever before, paying off your credit card debt can save you more money than ever before.

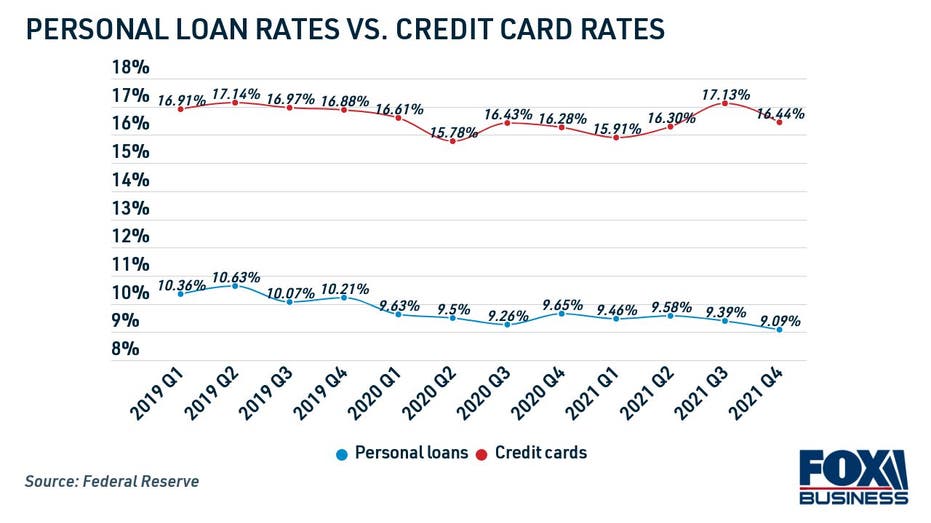

In the fourth quarter of 2021, the average two-year personal loan interest rate hit a record low of 9.09%, according to the Federal Reserve. During the same period, the average credit card rate for interest-rated accounts was much higher at 16.44%.

Continue reading to learn about credit card consolidation and visit Credible to compare personal loan rates for free without affecting your credit score.

Millions of Americans Fear Running Out of Debt Payments, NY FED Report

Consolidation Is Cheaper Than Ever Despite Soaring Credit Card Debt

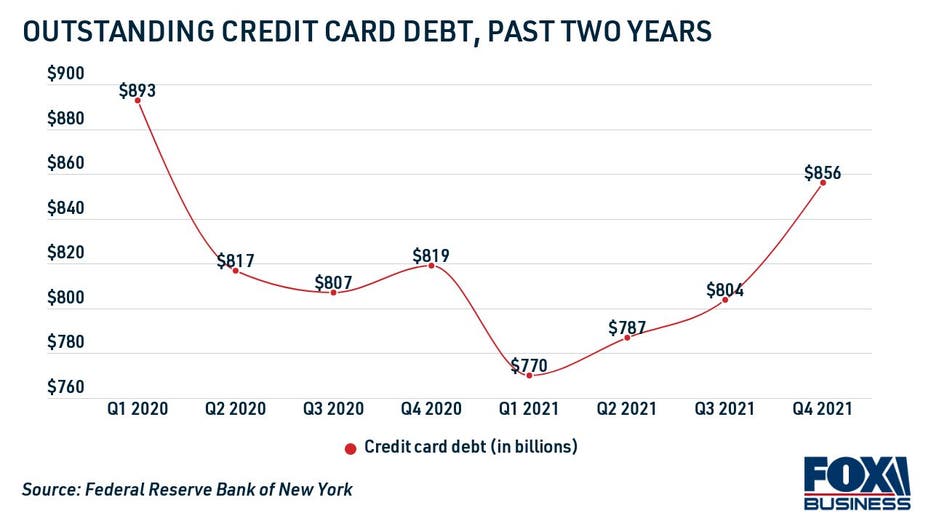

According to the Federal Reserve Bank of New York, Americans are becoming more and more dependent on credit cards as their debt balances skyrocket. Outstanding credit card balances increased 6.5% in the fourth quarter of 2021, taking consumer balances to his $52 billion.

With credit card balances skyrocketing, consolidating debt into low-interest personal loans is more profitable than ever.

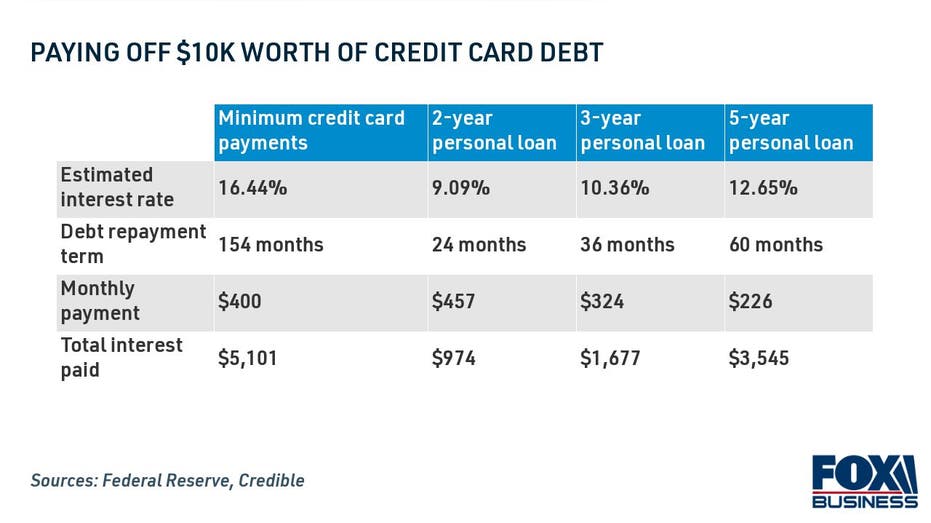

A recent analysis found that repaying $10,000 worth of credit card debt over a two-year personal loan at an interest rate of 9.09% would cost borrowers $4,000 more in interest compared to making the lowest credit card payment. estimated to save. By refinancing using this credit card repayment strategy, the borrower can pay off his balance ten years early by adding just $57 to his monthly payment.

You may also be able to save money over time and reduce your monthly payments by consolidating into a long-term personal loan. Please note that you may be able to get a fixed interest rate that is lower than what you are paying with your credit card.

For eligible applicants who took out a personal loan on Credible during the week of January 31st, the five-year average fixed personal loan interest rate was 12.65%. With the terms of these personal loans he could potentially be lower as he pays off $10,000 worth of credit card debt. A $174 reduction in monthly payments saves him over $1,500 during the repayment period.

Get a free personal loan repayment estimate on Credible and see how much you can save with our integrated credit card loan calculator.

How to get a balance transfer credit card

How to Consolidate Credit Card Debt with Personal Loans in 5 Steps

Using a personal loan for credit card debt consolidation can save you money while paying off your debt with predictable monthly payments. The process for applying for personal loans is as follows:

- Sum all credit card balances. This helps determine how much personal loan you need to borrow to pay off your credit card debt. You can combine one or more credit card balances into one personal loan payment.

- Check your credit score. Because personal loans are unsecured and do not require collateral, lenders use your credit history to determine risk and eligibility. Applicants with very good to excellent credit, defined by the FICO model as a credit score of 740 or higher, have the lowest personal loan interest rates.

- Check personal loan interest rates. Most lenders can verify loan terms, including estimated interest rates, through a soft credit check through a process called prequalification. Credible allows you to compare interest rates on personal loans from multiple lenders at once.

- Choose the best personal loan. Interest rates, loan fees, loan amounts, and loan terms should be taken into account when comparing offers. Once you have selected a lender, you will need to submit a formal application. This requires a hard credit investigation.

- Take a loan to pay off your credit card. If approved, you will receive your personal loan funds the next business day. You can usually deposit directly into your bank account. You can then use your personal loan balance to pay off your credit card.

How to check your credit report for free with no penalty

You can zero out your credit card balance, but it’s important not to add to your debt while paying off your personal loan. Paying off your credit card debt in full each month should always be your priority to avoid paying interest.

Visit Credible to learn more about debt consolidation loans from online lenders. Additionally, see current personal loan interest rates in the table below to determine if this method of debt repayment is right for your financial situation.

Balance transfer cards with 0% introductory period in April are rapidly disappearing

Have a financial question and don’t know who to ask? Email a Credible Money Expert moneyexpert@credible.com Your question may be answered by Credible in the Money Experts column.

[ad_2]

Source link