[ad_1]

key insight

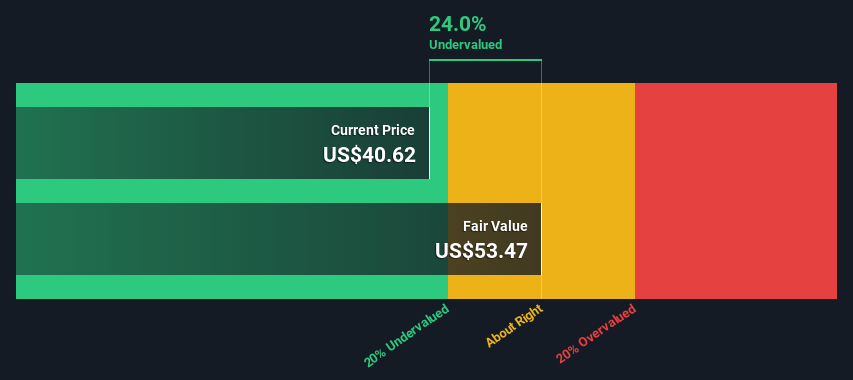

- The estimated fair value of Dell Technologies is $53.5 based on a two-phase free cash flow into the stock.

- Current stock price of $40.6 suggests Dell Technologies is undervalued by 24%

- DELL analyst price target of $48.73, 8.9% below fair value estimate

This article uses Dell Technologies Inc. (NYSE:DELL) forecasts future cash flows and discounts them to today’s value. For this purpose, we utilize the discounted cash flow (DCF) model. Such a model may seem incomprehensible to the layperson, but it is fairly easy to follow.

Note that there are many methods of evaluating a company and, like DCF, each method has its strengths and weaknesses in certain scenarios. If you want to learn a little more about intrinsic values, Simply the Wall St analytical model.

See the latest analysis from Dell Technologies

calculation

As the name suggests, we use a two-stage DCF model that considers two stages of growth. The first stage is generally a period of high growth that levels off towards the closing price captured in the second “steady growth” period. First, you need to estimate your cash flow over the next 10 years. We use analyst estimates when available, but if these are not available, we extrapolate previous free cash flow (FCF) from previous estimates or reported values. Over this period, we expect companies with shrinking free cash flow to contract at a slower rate, and those with growing free cash flow to see slower growth. This is to reflect that growth tends to slow in the early years rather than in later years.

In general, we assume that a dollar today is worth more than a dollar in the future, so the sum of these future cash flows is discounted to today’s value.

10-Year Free Cash Flow (FCF) Forecast

| 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | |

| Leverage FCF ($, million) | $795.6 million | $5.52 billion | $4.26 billion | $4.92 billion | $4.93 billion | $4.89 billion | $4.88 billion | $4.91 billion | $4.95 billion | $5.02 billion |

| growth rate source | 5 analysts | 6 analysts | 5 analysts | Analyst x 1 | Analyst x 1 | Est @ -0.97% | Est @ -0.09% | Est @ 0.53% | Est @ 0.97% | estimated @ 1.27% |

| Present Value ($, Millions) Discount @ 13% | $707 | US$4.44 million | US$3 million | $3.1 million | $2.7 million | US$2.4 million | $2.1 million | US$1.9 million | $1.7 million | $1.5 million |

(“Est” = FCF growth rate estimated by Simply Wall St)

10-Year Present Value of Cash Flows (PVCF) = $24 billion

The second stage, also called terminal value, is the cash flow of the business after the first stage. We use the Gordon Grosse formula to calculate the terminal value at a future annual growth rate equal to his 5-year average of 2.0% for 10-year Treasury yields. Discount the final cash flows to their present value at the 13% cost of equity capital.

Terminal value (TV)= FCF2032 × (1 + g) ÷ (r – g) = US$5 billion × (1 + 2.0%) ÷ (13%– 2.0%) = US$48 billion

Present Value of Terminal Value (PVTV)= television / (1 + r)Ten= US$48 billion ÷ ( 1 + 13%)Ten= $15 billion

Total value, or equity value, is the sum of the present value of future cash flows, in this case US$38 billion. Divide this by the total number of outstanding shares to get the intrinsic value per share. Compared to its current share price of US$40.6, the company appears a bit undervalued at a 24% discount to its current share price. However, evaluation is an imprecise tool, like a telescope. Move a few degrees and you’ll end up in another galaxy. Remember this.

Assumption

We point out that the most important inputs to discounted cash flows are the discount rate and, of course, the actual cash flows. You do not have to consent to these inputs. I encourage you to redo the calculations yourself and play with them. The DCF also does not give a complete picture of a company’s potential performance, as it does not take into account the cyclicality of the industry or the company’s future capital requirements. Given that we view Dell Technologies as a potential shareholder, the cost of capital is used as the discount rate rather than the cost of capital (or weighted average cost of capital, WACC) that accounts for the liability. For this calculation we used 13% based on a leverage beta of 1.763. Beta is a measure of a stock’s volatility relative to the market as a whole. Our betas are derived from industry average betas of globally comparable companies and are capped between 0.8 and 2.0. This is a reasonable range for a stable business.

Dell Technologies SWOT Analysis

- Debt is well covered by income.

- Revenue has declined over the past year.

- Dividends are low compared to the top 25% of dividend payers in the tech market.

- Annual revenue is projected to increase over the next four years.

- Good value based on P/E ratio and estimated fair value.

- Debt is not fully covered by operating cash flow.

- Total liabilities exceed total assets, increasing the risk of financial distress.

- Dividends are not included in cash flows.

- Annual revenue is projected to grow more slowly than the US market.

Future plans:

Valuation is just one aspect of the coin when it comes to making investment papers, and just one of the many factors by which a company should be evaluated. A DCF model cannot give foolproof estimates. Instead, the DCF model’s best use is to test certain assumptions and theories to see if they lead to a company being undervalued or overvalued. For example, a small adjustment to terminal value growth rate can dramatically change overall results. Can you see why the company is trading at a discount to its intrinsic value? There are three additional aspects of Dell Technologies that should be considered.

- risk: For a good example, we found Dell Technologies 6 Warning Signs You should know, and one of them makes us a little uncomfortable.

- future earnings: How does Dell’s growth rate compare to its peers and the wider market? Free analyst growth forecast chart.

- Other quality alternatives: Do you like all-rounders?expedition Our interactive list of high-quality stocks lets you know what else you might be missing!

PS. Simply Wall St updates his DCF calculations for all US stocks daily, so if you want to find the intrinsic value of other stocks, search.

Valuation is complicated, but we’re here to help make it simple.

find out if Dell Technologies You may be overestimated or underestimated by checking out our comprehensive analysis including: Fair value estimates, risks and warnings, dividends, insider trading and financial health.

View Free Analysis

Do you have feedback on this article? What interests you? contact directly with us. Or send an email to our editorial team (at) Simplywallst.com.

This article by Simply Wall St is general in nature. We provide comments based on historical data and analyst projections using only unbiased methodologies and our articles are not intended as financial advice. It is not a recommendation to buy or sell stocks and does not take into account your objectives or financial situation. We aim to deliver long-term focused analysis based on fundamental data. Please note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Is not …

[ad_2]

Source link